Can you realistically afford a home in Columbus right now?

Let’s get straight to it. If you are thinking about buying a home in Columbus, the real question is not just “how much does a house cost?” It is “how much income do I actually need to live comfortably after buying?”

That distinction matters.

Many buyers come into the market after browsing homes for sale in cincinnati ohio or comparing cincinnati homes for sale, assuming similar pricing means similar affordability. But income requirements depend on more than listing prices. They depend on your loan terms, lifestyle, and financial discipline.

So let’s break this down in a way that actually helps you make a decision.

What income do you need to buy a house in Columbus?

Here is the practical answer.

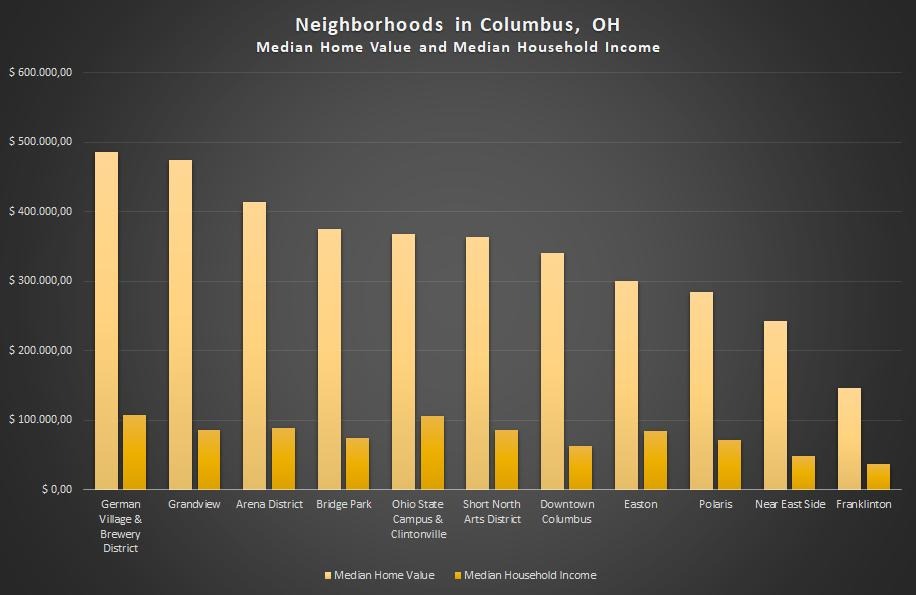

For a typical home in Columbus priced between 280,000 and 320,000 dollars, most buyers need an annual household income between: $65,000 and $95,000

That range assumes:

- A standard mortgage

- A moderate down payment

- Normal living expenses

Now, if your income is below that, it does not automatically mean you cannot buy. It just means you need to adjust expectations, either by lowering your price range or increasing your down payment.

Breaking down the numbers in real terms

Monthly affordability snapshot

| Category | Estimated Cost |

| Mortgage Payment | $1,400 to $2,100 |

| Property Taxes | $250 to $450 |

| Insurance | $100 to $200 |

| Utilities | $150 to $300 |

| Total Monthly Housing | $1,900 to $3,000 |

Financial experts often recommend that your housing costs stay within 28 percent to 32 percent of your gross income.

So if your total monthly housing cost is around $2,400, you should ideally earn about $7,500 per month, which translates to roughly $90,000 annually.

That is where the income range comes from.

Why Columbus is still considered affordable

Columbus continues to attract buyers because it offers a rare balance. Home prices are still within reach, while job opportunities remain strong. The presence of institutions like Ohio State University keeps the local economy stable and growing.

Compared to cities where entry level homes already exceed half a million dollars, Columbus gives buyers a chance to enter the market without extreme financial pressure.

This is exactly why many people who initially explore houses for sale in cincinnati ohio begin to consider Columbus as a smarter long term move.

Real world scenarios: what buyers actually earn

Let’s make this practical.

Scenario 1: First time buyer

A couple earns a combined income of $70,000 per year. They purchase a home priced at $260,000 with a modest down payment.

Their monthly payment stays manageable because they choose a slightly lower price range. They live comfortably and still have room for savings.

Scenario 2: Mid income professional

An individual earning $85,000 buys a $300,000 home. Their monthly payments are higher, but still within a safe range. Over time, they build equity while maintaining financial stability.

Scenario 3: Investor mindset

An investor earning over $100,000 looks at Columbus not just as a place to live, but as an opportunity. Instead of renting, they buy a property that can generate future rental income.

Many investors who once searched for a house for rent cincinnati ohio or tried to rent a house cincinnati begin shifting their focus toward ownership in Columbus for this exact reason.

Renting vs buying: how income plays a role

At first glance, renting feels easier.

In Columbus, rent typically ranges between $1,200 and $1,800 per month. That means you can live in a decent property without needing a large upfront investment.

But over time, renting becomes expensive in a different way. You are paying every month without building ownership.

Buying, on the other hand, turns your monthly payment into long term value. Your income is not just covering a cost. It is building equity.

That is why many people transition from searching houses for rent in cincinnati ohio to seriously evaluating buying options in Columbus.

How to calculate your personal affordability

This is where most buyers need clarity.

Start by looking at your monthly income before taxes. From there, apply the 30 percent rule. That gives you a safe estimate of what you can spend on housing.

Then factor in your existing debts, lifestyle expenses, and savings goals.

What you will notice is this. Two people with the same income can afford very different homes depending on how they manage money.

That is why income alone does not tell the full story. Your financial habits matter just as much.

Expert guidance: how to increase your buying power

If you are close to your target income but not quite there, there are ways to improve your position.

A larger down payment can significantly reduce your monthly burden. Improving your credit score can also lower your interest rate, which directly impacts affordability.

Another approach is to start slightly below your maximum budget. This gives you breathing room and reduces financial stress.

The goal is not to buy the most expensive home you qualify for. The goal is to buy the right home for your situation.

Is Columbus a good place to invest in property?

The short answer is yes, but only if you approach it with a clear strategy.

Columbus offers steady population growth, a strong rental market, and moderate entry prices. These factors create a solid foundation for long term investment.

Investors who once focused heavily on cincinnati homes for sale are now expanding into Columbus because the numbers make sense. Rental demand is consistent, and appreciation is steady rather than volatile.

For investors, the real advantage is balance. You are not relying on rapid price spikes. You are building sustainable returns.

Common mistakes buyers should avoid

One of the biggest mistakes is overestimating affordability. Just because a lender approves a certain amount does not mean it is the right decision.

Another common issue is ignoring hidden costs. Maintenance, insurance, and taxes can quietly add hundreds of dollars to your monthly expenses.

Some buyers also rush into decisions based on emotion. A house might look perfect, but if it stretches your finances too thin, it can become a burden rather than an asset.

Taking a step back and evaluating the full picture always leads to better outcomes.

Where to go from here

If you have been exploring houses for sale in cincinnati ohio or even considering a house for rent cincinnati ohio, this might be the right moment to rethink your strategy.

Columbus offers a strong entry point into homeownership, especially for buyers who want long term value rather than short term convenience.

The key is to approach the process with clarity, patience, and a clear understanding of your financial position. And as you move forward, keep this mindset in focus:

Invest in yourself. Invest with us.

Final thoughts

Buying a home in Columbus is not just about hitting a certain income number. It is about aligning your income with your lifestyle, your goals, and your long term financial vision.

For most buyers, an income between $65,000 and $95,000 creates a comfortable path into homeownership. But smart planning can open the door even earlier.

Columbus continues to stand out because it offers opportunity without overwhelming risk. That balance is rare, and it is exactly what makes it worth serious consideration.

If you are ready to take the next step, start exploring your options, run your numbers carefully, and move with confidence.

Frequently Asked Question

What is the minimum income to buy a house in Columbus?

Most buyers need at least $60,000 annually, but this depends on home price, loan terms, and debt.

Can I buy a home in Columbus with $70K income?

Yes, many buyers in this income range successfully purchase homes by choosing the right price range.

Is Columbus cheaper than Cincinnati for buyers?

In many cases, yes. Columbus often offers better long term value and job growth.

Is renting better than buying in Columbus?

Renting offers flexibility, but buying builds equity and long term financial stability.

How can I afford more expensive property?

Improving credit, increasing your down payment, and reducing debt can all increase your buying power.